As crypto markets mature and institutional participation deepens, governments are moving in sharply different directions when it comes to regulation. The European Union, the United Kingdom, and the United States now represent three distinct regulatory models, each shaped by its legal tradition, risk tolerance, and view of crypto’s role within the broader financial system.

These differences are no longer theoretical. Regulation increasingly determines where exchanges operate, where startups incorporate, and how investors assess jurisdictional risk. For market participants, understanding how the EU’s Markets in Crypto-Assets framework, the UK’s Financial Conduct Authority regime, and the fragmented U.S. approach diverge has become essential.

Why global crypto regulation is diverging

Crypto has moved beyond its early experimental phase. Stablecoins are now used for payments and settlement, exchange-traded funds have integrated Bitcoin into traditional portfolios, and major financial institutions offer custody, trading, and research services. Governments are responding to this shift, but their responses reflect fundamentally different regulatory philosophies.

In Europe, lawmakers have opted to codify crypto rules directly into law, prioritizing legal certainty and harmonization. In the United Kingdom, regulators have taken a more restrictive, permissions-based approach aimed at limiting consumer exposure. In the United States, crypto oversight has evolved largely through enforcement actions and court decisions rather than comprehensive legislation.

The European Union: MiCA and legal certainty by design

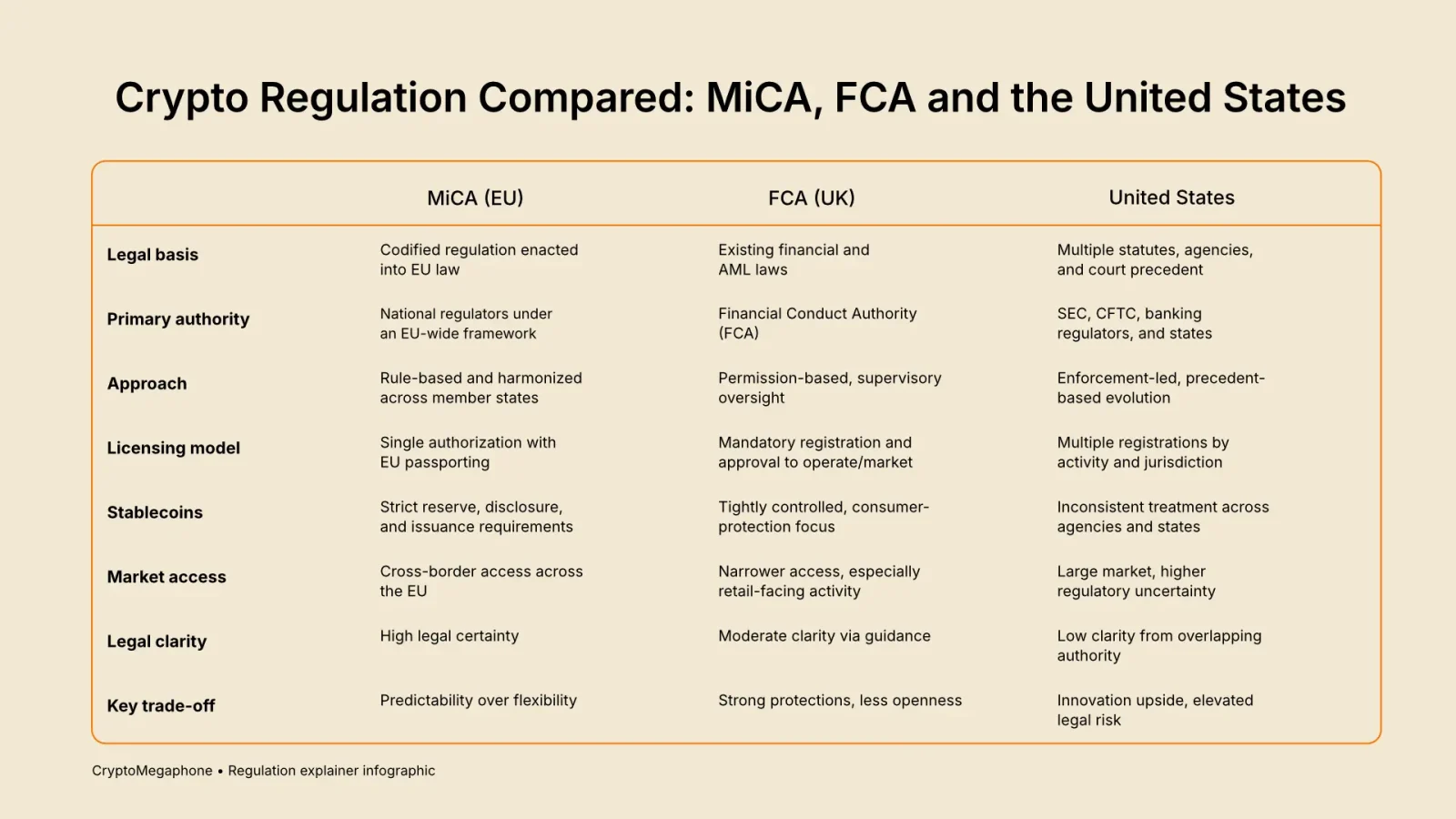

The European Union’s Markets in Crypto-Assets Regulation, commonly known as MiCA, represents the most comprehensive crypto framework enacted by a major economic bloc to date. Instead of relying on regulatory interpretation or case law, MiCA establishes crypto rules explicitly within EU legislation.

Under MiCA, crypto-asset service providers are subject to a single licensing regime that applies across all 27 EU member states. Once authorized in one jurisdiction, firms are permitted to operate throughout the bloc under passporting rules. The regulation introduces standardized requirements for custody, governance, capital reserves, and disclosures, while also defining specific categories for different types of crypto assets.

Stablecoins receive particular scrutiny under the framework. Issuers are required to maintain sufficient reserves, meet transparency and redemption standards, and comply with limits designed to mitigate systemic risk. European policymakers have consistently framed these measures as necessary safeguards for financial stability rather than barriers to innovation.

The principal advantage of MiCA lies in predictability. Firms operating in the EU can clearly identify which activities are permitted, which authority supervises them, and what compliance standards apply. The trade-off is reduced flexibility. Critics argue that a rule-based system may struggle to adapt quickly to technological change, particularly in decentralized finance. Nonetheless, for institutions and long-term builders, MiCA offers a level of legal clarity that remains rare in the crypto sector.

The United Kingdom: FCA oversight and controlled market access

The United Kingdom has chosen a markedly different route. Rather than introducing a single, comprehensive crypto law, Britain regulates the sector primarily through the Financial Conduct Authority using existing financial regulations.

Crypto firms that wish to operate in or market to UK users must register with the FCA, particularly under anti-money laundering rules. In practice, this process has proven highly restrictive. A significant proportion of applicants have failed to secure approval, while others have withdrawn applications amid stringent compliance requirements and prolonged reviews.

The UK has also imposed strict controls on crypto promotions. Marketing communications must meet high standards of clarity, include prominent risk warnings, and, in many cases, be approved by authorized entities. These rules have significantly curtailed retail-facing crypto advertising and limited the ability of firms to promote products domestically.

Supporters of the FCA’s approach argue that it prioritizes consumer protection and market integrity in a sector known for volatility and misconduct. Critics counter that the regime risks pushing innovation offshore, particularly as global competitors offer more predictable regulatory environments. The UK model is cautious and deliberate, but it has resulted in a narrower crypto market.

The United States: fragmented authority and enforcement-led regulation

The United States presents the most complex and uncertain regulatory environment among major crypto markets. Unlike the EU, it lacks a unified federal framework, and unlike the UK, authority is divided across multiple agencies.

The Securities and Exchange Commission, the Commodity Futures Trading Commission, federal banking regulators, and state-level authorities all claim overlapping jurisdiction. This fragmentation has created uncertainty around core questions, including which tokens qualify as securities and which regulator has primary oversight.

In the absence of clear legislation, U.S. crypto regulation has largely evolved through enforcement actions, settlements, and court rulings. High-profile cases against exchanges, issuers, and service providers have shaped market behavior, often retroactively. While these actions establish precedents, they rarely provide comprehensive guidance for future compliance.

Congress has debated multiple crypto-related bills, but political divisions and jurisdictional disputes have slowed progress. As a result, many firms operate under legal risk rather than legal certainty, balancing access to deep capital markets against the possibility of regulatory intervention.

How the three regulatory models compare

The contrast between these jurisdictions reflects deeper structural differences. The European Union relies on codified law and harmonization, the United Kingdom emphasizes controlled access through regulatory discretion, and the United States continues to shape policy through enforcement and litigation. Each model offers distinct advantages and drawbacks depending on a firm’s risk tolerance, target market, and long-term strategy.

Implications for crypto companies

Regulatory divergence is increasingly shaping corporate decisions. Firms seeking predictability and cross-border access often view the EU as an attractive base. Those operating in the UK face a narrower but tightly supervised market. In the United States, companies gain access to significant capital and institutional demand, but must navigate persistent regulatory ambiguity.

Many global operators now adopt jurisdiction-specific strategies, tailoring products, disclosures, and market offerings to comply with local requirements rather than pursuing a uniform global model.

Implications for investors

For investors, regulation has become a material factor in assessing risk. Jurisdictional clarity influences exchange reliability, stablecoin design, and the legal status of assets. Markets governed by clear rules may offer lower counterparty risk, while uncertain environments can amplify volatility and legal exposure.

A regulatory crossroads for crypto

The divergence between MiCA, the FCA, and U.S. regulators underscores how differently governments perceive crypto’s role in the financial system. Europe has opted for codification, the UK for restriction and supervision, and the United States for enforcement-led oversight.

As crypto continues to integrate into global finance, these approaches may converge or diverge further. For now, regulatory geography is becoming as important as technological innovation in shaping the industry’s future.